FRESNO, Calif. – Fresno businesses are facing an insurance crisis as wildfire risks drive up premiums across California. Skyrocketing rates and widespread policy nonrenewals are making affordable coverage increasingly difficult to secure, threatening Fresno’s commercial sector.

According to Bill Avakian, owner of Avakian Insurance, the worst may be yet to come. “We’re not hearing the full story of how bad it’s going to be,” he warned, citing financial fallout from the January 2025 Southern California wildfires.

Avakian has firsthand experience with fire damage. “Two days after getting the keys to our building, a major fire set us back,” he recalled. The blaze, caused by Fourth of July celebrations, underscores the unpredictable risks business owners face.

Older Commercial Buildings Face Higher Insurance Costs

Beyond wildfires, aging infrastructure is another major driver of premium hikes, said Avakian. Many business owners don’t realize insurers are increasingly reluctant to cover buildings over 15 years old due to fire risks. “The condition of commercial buildings is deteriorating, and insurers are taking notice,” he explained.

Fresno’s real estate market still reflects the effects of the 2008 financial crisis, which slowed construction. With fewer new buildings since 2010, many businesses now occupy older properties, making them more vulnerable to rising insurance costs. While new developments are emerging north of Herndon and at Fresno State’s Campus Pointe, they don’t offset the growing number of aging properties.

Skyrocketing Insurance Premiums Are Reshaping Fresno’s Business Landscape

Fresno businesses have seen insurance premiums increase by as much as 500% in just six years. Below is a snapshot of actual insurance costs for various commercial properties in 2018 and 2024:

These staggering rate hikes are forcing many businesses to make tough financial decisions. Some may attempt to pass costs onto customers, while others—particularly those operating in older buildings—face the risk of shutting down altogether.

How Fresno Businesses Can Navigate the Crisis

Avakian advises business owners to prepare for continued increases. “This crisis isn’t going away anytime soon,” he cautioned. While upgrading commercial roofs can lower premiums, the steep upfront cost makes it unrealistic for many small businesses. “Newer buildings, especially with updated roofs, pay significantly lower premiums, but many businesses can’t afford the investment,” he said.

Fresno’s insurance crisis extends beyond individual policyholders. Rising costs could slow economic growth, cause job losses, and deter commercial investment—especially in areas where aging infrastructure makes coverage prohibitively expensive. Without reforms, Fresno risks losing both established businesses and future entrepreneurs.

Legislative Solutions for Fresno and California’s Insurance Crisis

At a recent Fresno Chamber of Commerce Board of Directors meeting, State Policy Advocacy Director Peter Ansel outlined potential solutions for California’s struggling insurance market. He emphasized the urgent need for reform, stating:

“California’s insurance market cannot thrive unless we implement more effective risk assessments, improve prevention strategies, and build a stronger workforce to handle the increasing demand. We need immediate action to reverse the current trends and ensure long-term stability.”

In response to Fresno’s insurance challenges, local leaders can take proactive steps to support businesses. This includes expanding relief programs for aging infrastructure, advocating for localized risk assessments, and pushing for reforms to Proposition 103 to allow more flexible rate adjustments. Additionally, increasing workforce training programs and streamlining the FAIR Plan exit process at the state level would provide businesses with more coverage options.

The Current Insurance Crisis

Wildfires in Los Angeles and Ventura counties have highlighted California’s escalating risks. As fires become more frequent and severe, insurers are retreating from high-risk areas, leaving businesses scrambling for coverage.

California’s insurance market is struggling with supply chain disruptions, rising material costs, and inflation. If not for the high risk, the state’s large market would be highly attractive to insurers. However, financial stability takes priority, forcing companies to limit exposure.

“Seven of California’s top 12 insurance providers, covering 85% of the market, have either discontinued or significantly limited policies,” said Peter Ansel, Director of State Policy Advocacy of the California Farm Bureau at a Fresno Chamber of Commerce Board of Directors Annual Retreat. Insurers must first ensure their own financial stability in order to continue to protect policyholders.

Mass Policy Cancellations Leave Businessowners Scrambling

As insurers retreat from high-risk areas, businesses are facing an alarming rise in policy cancellations. Over the past year, tens of thousands of Californians have received non-renewal notices, mainly for home policies, particularly in wildfire-prone regions like the Sierra Nevada foothills, parts of Los Angeles County, and the Bay Area’s wildland-urban interface zones.

For many, securing a new policy has proven nearly impossible. Even those who manage to find coverage are often met with significantly higher premiums and reduced benefits. This has placed immense financial strain on property owners and left some unable to sell or refinance their homes due to insurance requirements.

The trend of mass cancellations has accelerated the shift toward California’s insurer of last resort—the FAIR Plan. When the crisis started, agricultural landowners and businesses were even trickier to cover because if they were non-renewed, they were precluded from accessing even the FAIR Plan. The California Farm Bureau sponsored Senate Bill 11, signed by the Governor in 2021 which updated that law.

To protect homeowners directly impacted by wildfire, California Insurance Commissioner Ricardo Lara has imposed a temporary mandatory moratorium preventing insurance companies from canceling or non-renewing residential property policies in wildfire-affected areas. However, this measure is not a long-term solution.

What Is the FAIR Plan?

The California FAIR Plan (Fair Access to Insurance Requirements) serves as an insurer of last resort, offering coverage to homeowners and business owners who cannot obtain private insurance. Originally designed as a small-scale safety net, the FAIR Plan has experienced unprecedented growth as private insurers continue to withdraw from the market.

While the program provides critical coverage for those in high-risk areas, it is not a state-run agency. Instead, the FAIR Plan functions as a fire insurance pool funded by all licensed insurers in California. Despite being a temporary solution, it has become increasingly relied upon as traditional insurance options diminish.

FAIR Plan Growth: A Sign of Market Instability

In 2020, the FAIR Plan accounted for less than 3% of all homeowner and business policies in California. By 2024, residential policies under the plan skyrocketed by 123%, reaching approximately 451,799 policies, while commercial policies grew by 161% totaling 13,101 policies.

Notably, farm policies are disproportionately high, comprising 6% of FAIR Plan policies compared to just 2% in the standard insurance market. This disparity indicates that even though agricultural properties often have a lower risk for wildfire propagation, because they have managed vegetation, irrigation, plowed, and cultivated lands, they face non-renewals at the same rate as other parcels in that region.

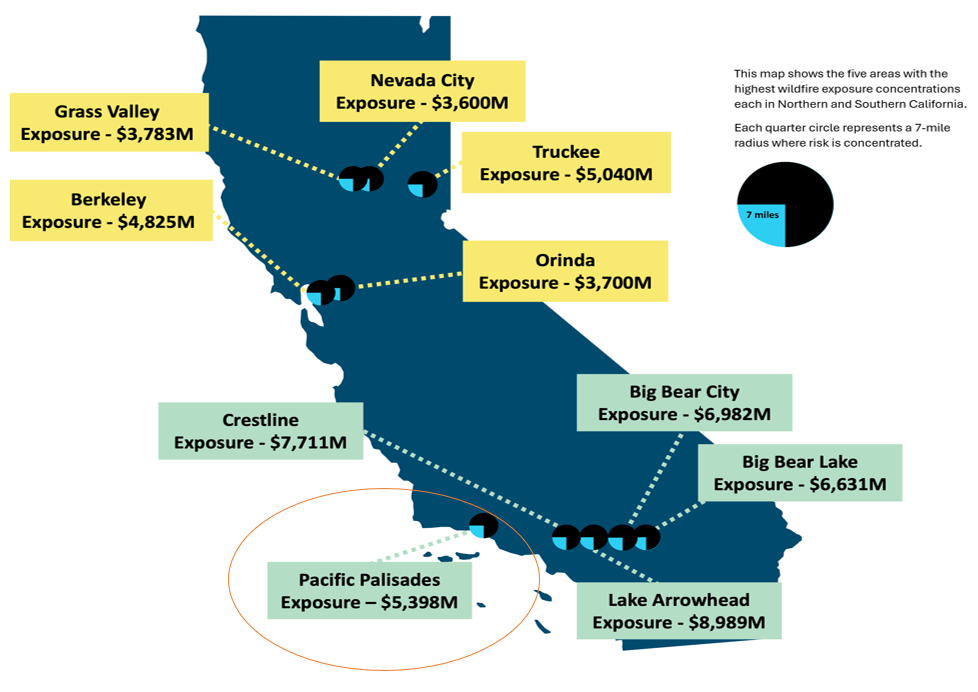

Wildfire Hotspots: Billions in Exposure

California’s top wildfire-exposed areas include Lake Arrowhead, Nevada City, Orinda, Grass Valley, and the Palisades, with Lake Arrowhead ranking as the most at-risk. The Palisades alone has over $4 billion in exposure, while the Eaton Fire north of Pasadena accounts for $775 million. According to a FAIR Plan report, as of September 30, 2024, Fresno’s total insurance exposure—including residential, commercial, and business owner policies—stands at $3.7 billion. If another major wildfire ignites in these high-risk zones, the FAIR Plan could face financial collapse.

The economic impact of California wildfires is staggering. For example, the 2018 Camp Fire in Paradise, California, cost insurers $12.5 billion, leading to significant premium hikes and widespread policy cancellations. This underscores the challenge of maintaining a sustainable insurance market in wildfire-prone areas.

To find out if your county or zip code is protected by a moratorium, click here.

Click here to see residential, commercial, and business owner’s exposure by county.

California’s Insurance Commissioner’s Plan to Address Wildfire Risks

Acknowledging the urgency of the situation, California Insurance Commissioner Ricardo Lara has outlined a strategy to address the state’s insurance crisis. His plan focuses on expanding private coverage in wildfire-prone areas while bolstering the FAIR Plan’s sustainability. This involves encouraging insurers to reenter the market through updated risk assessments and incentives, supporting fire mitigation programs to reduce risks and costs and increasing consumer education about wildfire preparedness and insurance options.

California’s Wildfire Prevention Goals: A Missed Target

“We’re still at a crawl stage with this,” said Ansel. “The state created a plan for a wildfire task force, but the goal was essentially for the federal government to treat half a million acres per year, with the state aiming for the same.” In 2023, there was approximately 700,000 acres treated; far below the set goal.

Despite a budget surplus, showing in the 2025-26 California Budget, released on January 10th, little progress has been made toward wildfire prevention and treatment. “This year, the budget shows an unexpected $17 billion surplus out of a $322 billion spending plan (budget), with around $325 million allocated for wildfire risk mitigation,” Ansel said. A group of fire scientists assembled by former Governor Brown issued the Venado Declaration and determined that the state needs to treat 5 million acres per year to adequately address wildfire risk.

Additionally, the California Air Resources Board (CARB) has determined that to meet the state’s climate goals, the state needs to treat up to 2.5 million acres—without even accounting for wildfire risk. CARB notes that approximately one in 4 of the state’s population live in a high-fire risk area. “With current mitigation costs working out to roughly $3500 per acre. The cost of treating 5 million acres would be approximately $18 billion,” Ansel emphasized.

Workforce Shortages Hamper Wildfire Prevention Efforts

Beyond funding concerns, a shortage of trained personnel is further slowing wildfire prevention. “To make this plan a reality, California would need to bolster its workforce. Butte Community College offers training for forestry and reforestation, but the state’s California Conservation Corps is not staffed to traditional levels. These hand crews are vital to the state’s mitigation and firefighting efforts,” Ansel added.

The concentration of risk in fire-prone areas makes the FAIR Plan financially vulnerable. Without meaningful reform and risk diversification, its ability to provide coverage remains uncertain. As wildfire threats intensify, so does the urgency for long-term solutions that ensure both accessibility and financial sustainability in California’s insurance market.

For more updates on Fresno County development and business initiatives, stay connected with the Fresno Chamber of Commerce.